An accountant friend of mine in Sydney told me last month that Division 7A is the single most common reason her small business clients get surprise tax bills. Not fraud. Not big mistakes. Just a director who borrowed money from their own company and never ran the numbers.

A Div 7A calculator prevents exactly that. It tells you the minimum repayment you must make each year so a company loan isn't suddenly taxed as a dividend. Here's how it works and how to use one properly.

What Is Division 7A?

Division 7A is an Australian tax rule that stops private companies from handing tax-free benefits to shareholders or their associates through loans, payments, or forgiven debts.

If these transactions aren't structured correctly, the tax office can treat them as dividends and tax them as personal income. That's the trap the whole rule is built around.

It applies to payments, advances of money, or debt forgiveness by private companies to shareholders or related persons. If a loan isn't repaid properly or fails the compliance rules on interest rate, term, and written agreement, the unpaid portion may be deemed a Division 7A dividend.

The rules have applied to amounts on or after 4 December 1997. In short, you must structure the loan correctly with an agreement, the right interest, and a repayment schedule to avoid it being taxed as a dividend.

Why This Matters More Than People Think

Here's the part that catches business owners off guard. A Division 7A breach doesn't just create a small penalty. The entire unpaid loan balance can be treated as assessable income in one hit.

Borrow $80,000 from your company, miss the compliance requirements, and you could face tax on the full $80,000 as a personal dividend. For a shareholder in a high tax bracket, that's a devastating bill from what felt like simply moving your own money around.

That's exactly why a calculator isn't optional busywork. It's the guardrail between a routine loan and a five-figure tax surprise.

Key Inputs You Need for the Calculator

Before running any Div 7A calculator, gather these details. Missing even one throws off the whole result.

Input | What It Means |

|---|---|

Opening loan balance | The outstanding amount at the start of the year |

Year the loan was created | The income year it began |

Secured or unsecured | Secured loans get longer terms |

ATO benchmark interest rate | The official rate for that specific year |

Loan term / remaining term | How long the loan runs |

Repayments made this year | Dates and amounts already paid |

Tax return lodgment date | Or the due date |

Multiple loans to amalgamate | Whether several loans combine into one |

These are the standard inputs across virtually every calculator and Excel model, so having them ready makes the process take minutes instead of hours.

How to Use a Div 7A Calculator Step by Step

The exact layout differs between tools, but the underlying logic stays identical. Here's the full process.

Step 1: Select the Income Year of the Loan

Step 1: Select the Income Year of the Loan

Choose the year the loan was first given, or when it was last amended if changes were made.

Step 2: Select the Year You're Computing For

Pick the current year or a prior year, depending on what you're checking.

Step 3: Enter the Opening Balance

Input the loan amount outstanding at the start of that year, before any repayments are applied.

Step 4: Enter Term and Type

For unsecured loans, the maximum allowable term is generally 7 years. Secured loans can stretch up to 25 years. Getting this wrong is one of the most common failures.

Step 5: Input the Benchmark Interest Rate

Use the rate the ATO set for that year. Most calculators include a dropdown so you don't have to look it up manually.

Step 6: Enter Any Repayments Made This Year

Add the dates and amounts already repaid. These reduce what you owe and lower your required minimum.

Step 7: Compute the Minimum Yearly Repayment

The calculator works out how much you must repay, both principal and interest, to stay compliant under Division 7A.

Step 8: Review the Outputs

You'll see the required repayment, closing balance, and interest breakdown clearly laid out.

Step 9: Verify Against Distributable Surplus

This is the step people skip. The deemed dividend cannot exceed the company's distributable surplus. If your required repayment exceeds that surplus, some amount may still be a deemed dividend.

Step 10: Make the Repayment or Adjust

If needed, pay the calculated amount before your tax return lodgment, or restructure the loan to avoid problems.

Many accounting suites include a Div 7A worksheet to automate this. BusinessFitness, for instance, includes a Div 7A starter or worksheet to compute interest and repayments.

Read Also: Verkada Pricing Guide: Costs, Features & Tips 2025

A Simple Worked Example

Let me show the calculator in action with clean numbers.

You have a loan given in 2021 for AUD 50,000. It's unsecured with a remaining term of 7 years. The benchmark interest rate is 7.5 percent, and no repayments have been made this year yet.

You input those values and the calculator returns the minimum repayment needed to avoid the loan being treated as a dividend. Pay that amount before lodgment and you stay compliant.

If you'd made partial repayments earlier in the year, the calculator adjusts the required amount downward, because less is owed overall.

A More Detailed Example

Here's a scenario closer to a real financial year.

A shareholder borrowed $50,000 on 1 July 2023 on an unsecured 7-year term. The benchmark interest rate is 8.27 percent for 2023 to 2024. During that year, they repaid $5,000 on 30 June 2024.

Inputting those values, the calculator shows three things: the minimum yearly repayment required, the interest due, and the new outstanding balance.

From there you can see clearly whether that $5,000 repayment was enough or whether more is still owed to stay compliant. That instant clarity is the entire point of the tool.

Benefits of Using a Div 7A Calculator

For accountants, business owners, and advisors dealing with private company loans, the practical upside is significant.

Accurate loan calculations determine the exact minimum yearly repayment required, cutting the risk of underpayment or non-compliance.

Time savings are real. Manually calculating interest, principal, and schedules eats hours. The calculator generates accurate results in seconds.

ATO compliance stays intact by aligning arrangements with benchmark rates and legislative requirements, preventing penalties and deemed dividend issues.

Simpler record keeping comes from downloadable summaries you can store for audit purposes.

Better financial planning follows from clear repayment timelines, letting businesses manage cash flow properly.

Fewer errors result from automation removing manual input mistakes and improving reliability across every calculation.'

Changes and Updates to Watch

Changes and Updates to Watch

Tax rules evolve, so a few moving parts deserve ongoing attention.

The ATO updates benchmark interest rates annually, which directly affects your repayment figures. For the 2025 to 2026 income year the benchmark rate sits at 8.37 percent, so always confirm the current year's rate before calculating.

Rules around Unpaid Present Entitlements and how trusts interact with Division 7A can shift over time. The concept of amalgamated loans, combining several loans into one for calculation, is often adjusted in updated rulings.

Legislative reforms may also modify maximum loan terms or interest concessions. For the most current guidance, always check the ATO website or a reputable tax advisor.

Common Mistakes and Pitfalls

Here are the errors that trip people up most, worth reading twice before you file.

Using the wrong interest rate instead of the official ATO benchmark. Missing repayments and blowing past the lodgment date, which triggers dividend treatment immediately.

Assuming secured versus unsecured terms incorrectly, like treating a loan as unsecured but running it past 7 years, which fails automatically. Not documenting the agreement, when a written loan agreement is mandatory.

Ignoring distributable surplus, since even correct repayments can't help if the company lacks enough surplus. Combining multiple loans incorrectly when they should be rolled into one amalgamated loan. And late lodgment inputs, where bonus or additional loans mid-year quietly change the calculation.

Always double-check your inputs and assumptions before treating any result as final.

Getting the compliance foundation right matters across every business tool, the same way login and access setup does for other platforms.

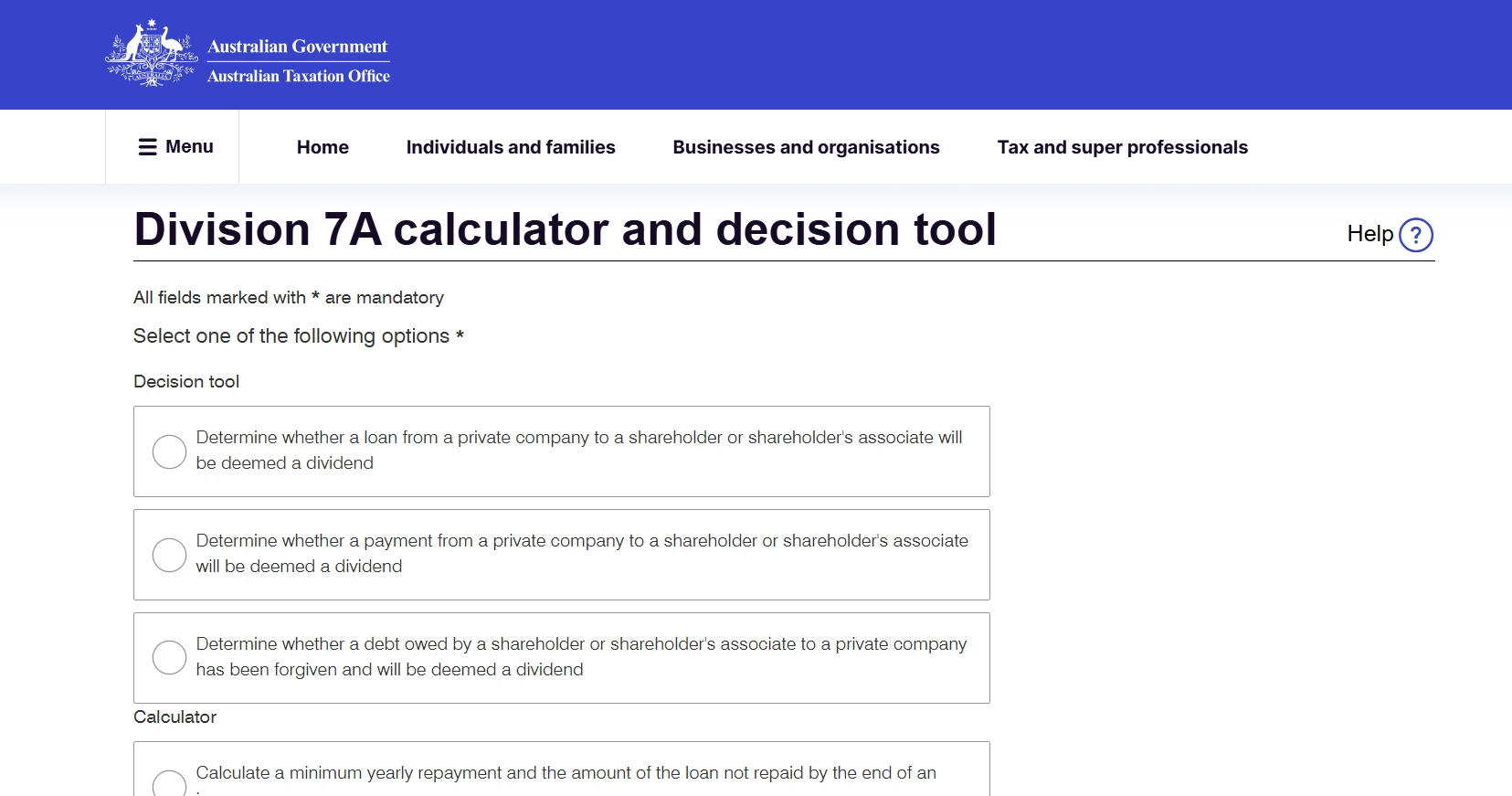

Div 7A Calculator Tools Available

Several trusted options exist, ranging from official to commercial.

Tool | Type | Notes |

|---|---|---|

ATO Division 7A calculator | Official | Compliance amounts and decision tool |

Thomson Reuters | Commercial | Previously offered a Div 7A loan calculator guide |

Digitax | Firm-hosted | Hosts calculators for minimum repayments |

BusinessFitness | Software worksheet | Company Debit Loan worksheet for interest and repayments |

The ATO's own Division 7A calculator and decision tool is the official reference and the safest starting point. Whatever you choose, pick a tool that's trusted, maintained, and updated, because tax rules and benchmark rates change every year.

Tips and Best Practices

A short checklist keeps you on the right side of the rules.

Always document the loan in writing at the time you make it. Keep records of all repayments including dates and amounts. Use the official ATO benchmark rate for each year, never an estimate.

Check distributable surplus before assuming you can repay fully. Run the calculator before each tax year to see required repayments. Make repayments before the company tax return lodgment date, or earlier if required.

If you're unsure, get advice from a tax specialist, since mistakes here are genuinely expensive. And update your calculations annually as the loan balance, interest rate, and term all shift.

Final Thoughts

A Div 7A calculator is essential for anyone dealing with private company loans to shareholders or their associates. It computes the minimum yearly repayment you need to keep a loan from becoming a deemed dividend, keeping your tax position clean and free of surprises.

Use the correct inputs, loan balance, term, benchmark rate, and repayments, then cross-check against distributable surplus. Use official or trusted tools, document everything, and review annually.

My accountant friend runs the calculator for every client with a company loan before lodgment season, without exception. That single habit has saved her clients from more painful tax bills than anything else she does. Treat it as your guardrail and it works exactly the same way for you.

FAQs

Is the Div 7A calculator mandatory?

No, but using one is the simplest way to determine minimum repayments and confirm compliance with ATO rules.

Can a loan become a deemed dividend?

Yes, if repayments or terms aren't met under Division 7A, the ATO can treat the loan as a taxable dividend.

How often should I use the calculator?

At least annually before your company tax return lodgment, and whenever new payments or repayments occur.

Does the calculator account for interest?

Yes, it applies interest based on the ATO benchmark rate for that financial year.

What if I miss the repayment deadline?

Part or all of the loan may be treated as a deemed dividend, triggering real tax consequences.